Featured

Table of Contents

Legal Defenses for Property Owners in the current housing market

The home loan environment in 2026 presents a complex set of difficulties for homeowners who have fallen back on their month-to-month payments. Economic shifts have led to a renewed focus on customer rights, especially for those dealing with the threat of losing their homes. Federal and state laws have progressed to guarantee that the foreclosure procedure is not an immediate or automated result of a few missed payments. Instead, the law mandates a series of procedural steps developed to provide debtors every opportunity to discover an alternative.In local communities throughout the country, the primary line of defense for a homeowner is the 120-day guideline. Under federal regulations preserved by the Customer Financial Protection Bureau (CFPB), a home mortgage servicer typically can not make the first legal declare foreclosure until a customer is more than 120 days overdue. This period is planned for the customer to send a loss mitigation application. If a complete application is received throughout this time, the servicer is restricted from starting the foreclosure procedure till the application is completely evaluated and a choice is made.The 2026 regulatory environment likewise strictly forbids "double tracking." This happens when a bank continues to move on with a foreclosure sale while at the same time thinking about the homeowner for a loan adjustment or a brief sale. In many jurisdictions, courts have ended up being progressively critical of loan providers who stop working to abide by these stops briefly. Homeowners who find themselves in this position typically search for Bankruptcy Alternatives to assist them validate that their rights are being appreciated by their loan servicers.

The Function of HUD-Approved Counseling in 2026

Navigating the paperwork required for loss mitigation is often the most considerable hurdle for those in the residential sector. For this factor, the federal government continues to fund and support HUD-approved real estate therapy agencies. These companies, such as APFSC, serve as a bridge between the debtor and the loan provider. As a DOJ-approved 501(c)(3) nonprofit, APFSC offers these services nationwide, guaranteeing that people in every metropolitan area have access to professional assistance without the high expenses of personal legal firms.HUD-approved therapists assist house owners understand the particular kinds of relief readily available in 2026. This may consist of a loan adjustment, where the loan provider changes the terms of the initial mortgage to pay more affordable. Other choices consist of forbearance, where payments are briefly suspended or reduced, and repayment plans that enable the homeowner to catch up on financial obligations over a set duration. Counselors likewise supply an unbiased take a look at whether a brief sale or a deed-in-lieu of foreclosure is a better course to avoid a shortage judgment.Financial literacy education is a cornerstone of this process. Lots of individuals dealing with insolvency in 2026 gain from a deep dive into their family spending plan to see where changes can be made. Peoria Debt Relief Services uses a structured path for those who are also struggling with high-interest credit card debt or other unsecured obligations that are draining pipes the resources required for their home mortgage. By consolidating these payments into a single lower quantity through a financial obligation management program (DMP), a property owner may discover the monetary breathing space necessary to keep their real estate status.

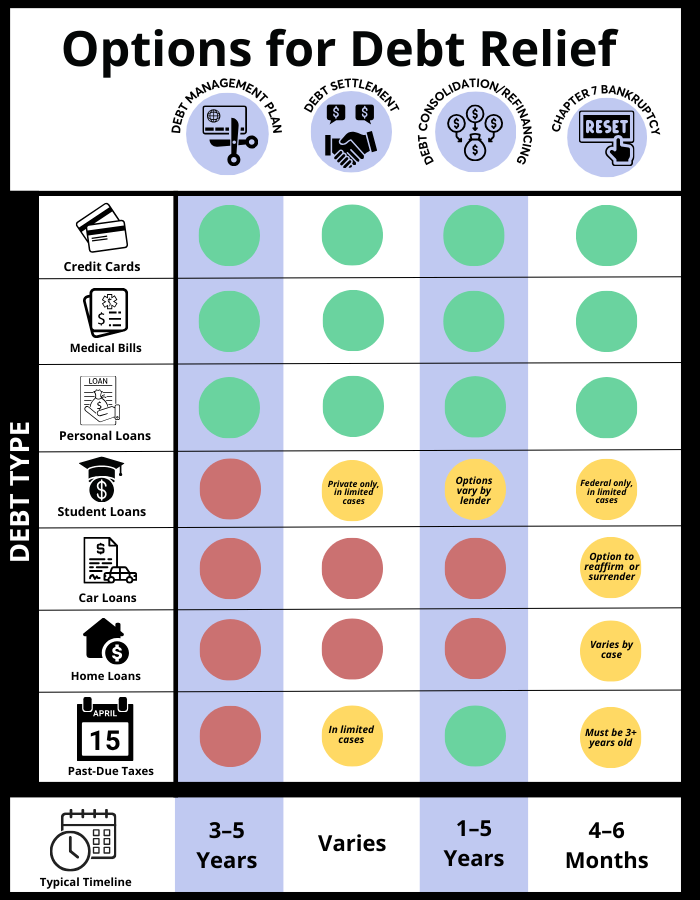

Browsing Insolvency and Debt Relief in the Local Market

When a property owner is faced with frustrating debt, the question of insolvency often causes a choice between a debt management program and an official personal bankruptcy filing. Both courses have considerable implications for a person's credit and long-lasting financial health. In 2026, the pre-bankruptcy counseling requirements remain a rigorous part of the U.S. Bankruptcy Code. Any individual wanting to declare Chapter 7 or Chapter 13 must initially complete a therapy session with an authorized company to figure out if there are feasible options to liquidation.Chapter 13 personal bankruptcy is regularly used by those in various regions who desire to keep their homes. It enables a reorganization of financial obligation where the homeowner can repay the missed home loan payments over a three-to-five-year duration. This is a legal process that stays on a credit report for up to seven years. In contrast, a financial obligation management program negotiated by a nonprofit like APFSC can often accomplish similar results for unsecured financial obligations without the serious effect of a personal bankruptcy discharge.Residents who are looking for Debt Relief in Peoria typically discover that a combination of real estate counseling and debt management provides a more sustainable healing. These programs include the firm negotiating straight with financial institutions to lower rates of interest and waive charges. This lowers the overall monthly outflow of cash, making it possible for the house owner to meet their main responsibility: the home mortgage. It is a proactive technique that attends to the origin of the monetary distress instead of simply dealing with the sign of a missed house payment.

Particular Protections Versus Unreasonable Servicing Practices

In 2026, new rules have actually been implemented to secure homeowners from "zombie foreclosures" and servicing mistakes. A zombie foreclosure takes place when a loan provider begins the process, the property owner moves out, but the lender never ever actually completes the sale. This leaves the previous resident responsible for property taxes, maintenance, and HOA costs on a home they no longer think they own. Modern securities in the local area now require loan providers to provide clearer notices regarding the status of the title and the house owner's ongoing responsibilities until the deed is officially transferred.Servicers are also held to greater requirements concerning "Followers in Interest." If a property owner passes away or a home is moved through a divorce settlement in any community, the new owner has the legal right to get details about the account and request loss mitigation. This guarantees that a family member who inherits a home can remain in it if they can demonstrate the ability to pay, even if their name was not on the original mortgage note.Furthermore, the 2026 updates to the Fair Financial Obligation Collection Practices Act (FDCPA) and the Fair Credit Reporting Act (FCRA) provide extra layers of security. If a servicer offers unreliable details to credit bureaus throughout a foreclosure dispute, property owners have the right to a speedy correction process. Not-for-profit credit therapy agencies play a function here too, assisting consumers review their credit reports for errors that could be preventing their capability to refinance or secure a brand-new loan.

Educational Requirements and Post-Discharge Recovery

For those who do go through a personal bankruptcy procedure, the law in 2026 needs a 2nd step: pre-discharge debtor education. This course is designed to supply the tools needed to manage financial resources after the legal proceedings are over. APFSC is authorized to offer both the preliminary pre-bankruptcy counseling and this final education action. The objective is to ensure that the insolvency occasion is a one-time occurrence which the individual can restore their credit and move toward future homeownership or financial stability.The focus of these academic programs is on long-lasting budget plan management and the smart usage of credit. In 2026, the rise of digital financial tools has made it much easier to track costs, however it has actually also made it simpler to accumulate debt through "buy now, pay later on" services and other high-interest customer products. Credit therapists work with individuals in their local surroundings to build an emergency situation fund, which is the most reliable defense versus future foreclosure.Homeowners are likewise motivated to take part in community-based financial literacy programs. APFSC often partners with local nonprofits and banks to provide these resources for free. By comprehending the rights offered under the 2026 housing laws and making use of the services of a HUD-approved counselor, residents can navigate even the most tough monetary periods with a clear plan.

The Significance of Early Action

The most constant advice from real estate professionals in 2026 is to act early. A mortgage servicer is far more most likely to use a favorable adjustment when the debtor connects before numerous payments have actually been missed. Once a foreclosure sale date is set, the alternatives become more limited and the legal expenses increase. In various municipalities, there are frequently regional mediation programs that need the loan provider to meet the customer in person, but these normally need to be asked for within a particular timeframe after the preliminary notice of default is sent.By dealing with an organization like APFSC, property owners can guarantee they are not going through the process alone. Whether it is through a financial obligation management program to clear up other monetary commitments or direct housing counseling to conserve a home, these 501(c)(3) companies supply the proficiency required to challenge unreasonable practices and secure a stable future. The consumer defenses in place for 2026 are strong, however they require the house owner to be proactive and informed. Understanding the law and using the readily available nonprofit resources is the finest method to prevent a temporary financial setback from becoming an irreversible loss of residential or commercial property.

{kind=link}

Latest Posts

Certified Counseling On Improving Credit Health for 2026

How to Locate Low Rate Personal Loans

Essential Financial Apps for Accurate 2026 Planning